Moving into aged care is rarely an easy decision. It often happens after a fall,…

How to stay in your home longer: A guide to government-funded home care services & options

“There is nothing like staying at home for real comfort” — Jane Austen.

As we age, the desire to remain in our own home surrounded by familiar routines, memories, and community grows stronger. But for many older Australians, the reality of staying at home becomes increasingly difficult due to health challenges, mobility issues, the complexity of navigating aged care services, and the growing financial strain from rising living costs while relying on a pension.

The importance of staying where you’re most comfortable

Image: Freepik

Being able to stay in your own home, where you feel safe, comfortable, and surrounded by everything familiar, is incredibly important as long as it’s safe to do so.

There are significant benefits to remaining in your local area and in the home you love, close to family and friends. According to the National Seniors Suitable Housing in Later Life survey, 70% of respondents believed their home would be suitable for them in later life, while 19% said it would not.

“I want my own base to live and feel grounded,” said one survey respondent.

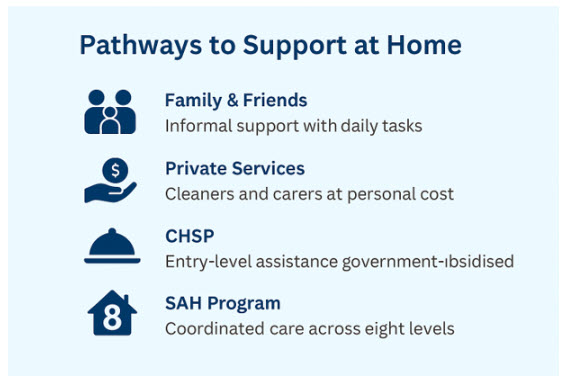

There are four key pathways to help older Australians stay at home longer. Family and friends often provide informal support with daily tasks, while private services like cleaners and carers can be arranged at personal cost. Government-subsidised programs include the CHSP for entry-level assistance and the Support At Home Program, which offers coordinated care across eight levels.

The changes to the aged care system (government-subsidised services) are the biggest in 30 years and can be pretty complex and confusing, but the good news is?

With the right planning, support, and financial advice, staying at home longer is not only possible but also empowering. You can choose to pay privately for services, access government subsidies, or a combination of both.

Proposed government-funded home care services changes from November 1st 2025

- New Support at Home program: A new program will combine the current government-funded home care service options into eight ongoing categories of care packages to better meet the specific needs of individuals.

- Higher contribution fees: While clinical care will be fully covered by the government (up to the available budget of your care package), you may have to pay more for services like cleaning and gardening.

- Means-testing: Your contributions to home care will now be means-tested, taking into account both assets and income, according to Centrelink rules.

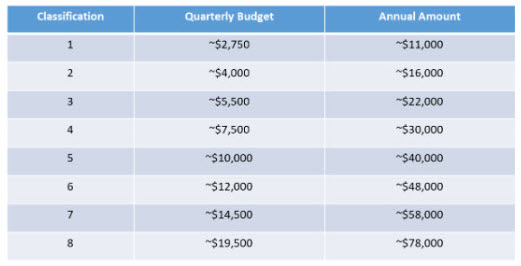

Classification and budgets for ongoing services

Support at Home will have eight classifications for ongoing services, replacing the four Home Care Package levels. Each classification will have a budget for participants to access services.

A new participant’s classification and budget will be determined at assessment based on their needs.

Existing Home Care Package clients and those waiting on the National Prioritisation System will not be reassessed into one of the new classifications when the new program starts.

They will be allocated a budget that aligns with their current Home Care Package level (or the level for which they have been approved and are awaiting access).

If their needs increase in future, they would be reassessed into a new Support at Home classification with a higher budget.

Annual Support at Home budgets are broken into quarterly (3-monthly) budgets.

Participants can carry over unspent funds of up to $1,000 or 10% of the quarterly budget (whichever is greater).

The indicative budget amounts for each ongoing classification are:

Assistive Technology and Home Modifications (AT-HM) Scheme

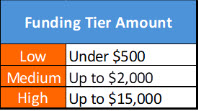

From 1 November 2025, the AT-HM Scheme will provide participants with access to assistive technology and/or home modifications without requiring them to save funds from their individual budgets.

The funding tiers are:

Assistive technology includes items, pieces of equipment or products that help a participant to:

- do things more easily

- complete activities they can no longer do independently.

Examples of assistive technology include:

- mobility equipment, such as walking sticks, walking frames and wheelchairs

- toileting supports, such as bedpans and commodes

- bathing devices, such as shower chairs and bath boards.

Home modifications involve altering a participant’s home environment to make it safer and more accessible.

Home modifications can include:

- Grab rails in the shower or bathroom

- internal and external handrails

- Ramps and stair lifts

- Bathroom redesign (e.g. changing the layout to improve accessibility)

- Widening doorways and passages (e.g. to allow for wheelchair access).

Restorative Care Pathway

The Restorative Care Pathway provides an intensive short-term period of care after an illness or injury to help you maintain or regain your independence.

Support will be available for up to 12 weeks (with the ability for a 4-week extension). This is an increase from the 8 weeks available under the STRC Programme.

The Restorative Care Pathway provides a budget of approximately $6,000 for the 16 weeks. If your restorative care provider determines that you require additional services within the 16 weeks, they can apply for up to an extra $6,000.

End-of-Life Pathway

The new End-of-Life Pathway will provide participants with three months or less to live with access to a higher level of in-home aged care services. This aims to help them stay at home for as long as possible.

An older person can be referred to a high-priority assessment to access the End-of-Life Pathway. They don’t need to be an existing Support at Home participant to be eligible.

Funding of up to $25,000 will be available, with a 16-week timeframe for utilising the funds.

For all Support at Home services, including the Restorative Care and End-of-Life Pathways, contributions apply for services delivered in the independence and everyday living service categories.

Participant contributions

Support at Home will focus government funding on care needs that will help participants to stay at home and avoid hospitalisations. Participants will make a greater contribution towards items they have paid for or provided for themselves their entire lives.

Participant contributions will be set at a rate per hour (or unit of service) at a set percentage for each service type. This means:

- The participant will pay the dollar amount set by the percentage

- The government will pay the remainder of the price, as a subsidy to the provider.

The rate will be based on the type of service received. Participants will make:

- No contribution for clinical support services (such as nursing and physiotherapy)

- Moderate contributions for independence services (such as personal care) and products, and equipment under the AT-HM Scheme. Many of these supports help keep participants out of the hospital and residential aged care.

- The highest contributions for everyday living services (such as domestic assistance and gardening) are typically not funded by the government for individuals at other stages of life.

The participant’s age pension status will determine individual contribution rates, with the:

- Lowest contributions for full pensioners

- Moderate contributions for part pensioners

- Highest contributions for self-funded retirees.

To protect self-funded retirees with lower incomes, participants eligible for a Commonwealth Seniors Health Card (CSHC) will have lower contributions than those who are not.

There will be a $130,000 lifetime cap on contributions to protect those who receive aged care for an extended period.

Transitional arrangements will apply for:

- Home care recipients

- Older people already approved for a package on 12 September 2024

- Older people already approved for a Home Care Package and listed on the National Priority System as of 12 September 2024.

The higher costs will primarily impact self-funded retirees and some part-pensioners. Still, everyone may face higher costs (and bigger decisions), making it essential to carefully choose care providers and understand their costs. The changes may simplify some of the confusion we’ve seen under the current system.

Now, more than ever, it’s essential to get advice to understand what you’ll need to pay and how these fees might change as your financial situation evolves.

Case study: Bill vs Sue—Same financial circumstance, different outcomes

Image: Freepik

*Modelled on HCP 4/SAH 5

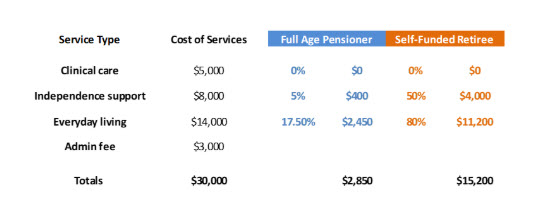

This document compares Bill’s and Sue’s costs under the current Home Care Package (HCP) system and the upcoming Support at Home (SAH) program, explaining the ‘no worse off’ principle with examples that assume both receive a Level 5 Support at Home package costing $40,000 annually.

| Feature | Home Care Package (Pre 12 Sept 2024) | Support at Home (From 1 July 2025) |

| Funding Model | Fixed HCP level funding | Coordinated care across 8 levels |

| Contribution Basis | Income-tested care fee (if applicable) | Percentage-based contributions by service type |

| Contribution Rates | Calculated under HCP rules | 0% clinical, 9.4% independence, 23.7% everyday living |

| Lifetime Cap | $82,018 (indexed) | $130,000 (indexed) |

| Transition Rule | Existing package retained | No worse off principle applies |

Part pensioner

Bill and Sue are independent single part pensioners. Bills and Sue’s individual incomes are $40,000 per year, including pension income of $25,260.

Bill and Sue own their home independently, and each has non-financial assets of $100,000.

Bill was approved and is in a home care package as of 12 September 2024; Sue is a new entrant. When SAH begins on 1 November 2025, Bill’s income will undergo an income and assets test for aged care, and he will pay the ‘no worse off principle’ contribution rates required.

Based on the aged care financial assessment, Bill and Sue’s contribution rates from 1 November 2025 will be:

| Service Type | Bill & Sue’s Contribution Rate | Bills Annual Cost (Assuming $40,000 package) |

| Clinical Services | 0% | $0 |

| Independence Services | 9.40% | $3,760.00 |

| Everyday Living Services | 23.70% | $9,480.00 |

Under the upcoming Support at Home program, clients like Bill who are already on a Home Care Package before 12 September 2024 will transition under the ‘no worse off’ principle. This means Bill will keep her current package level and funding amount, even though contribution rates will change under SAH.

For example, if Bill currently pays contributions based on HCP rules, he will not be required to pay more than that amount after 1 July 2025. His new rates under SAH would be 0% for clinical services, 9.4% for independent living services, and 23.7% for everyday living services, but capped so that his costs do not exceed previous levels. Bill will retain the current HCP lifetime cap amount (currently $82,018, indexed) and maintain the same HCP package amount.

As a new entrant, Sue will have a lifetime cap of $130,000 (indexed) under SAH, exposing her to a potential additional contribution of $47,982 over the life of her Age Care services.

Lesson: Your financial situation significantly affects your out-of-pocket costs. Strategic financial advice can help reduce these contributions and stretch your care budget further.

Lesson: Your financial situation significantly affects your out-of-pocket costs. Strategic financial advice can help reduce these contributions and stretch your care budget further.

Why planning ahead matters

Waiting lists for higher-level SAH packages can be long, sometimes up to 15 months. Applying early and understanding your options is crucial.

“By failing to prepare, you are preparing to fail” — Benjamin Franklin

How to choose a quality home care provider

Selecting and comparing providers can be overwhelming. You want a provider that delivers high-quality care and takes the time to understand your unique needs.

Here are 10 questions to ask when choosing a provider:

- What do you value? Do their values align with yours and your quality of life goals?

- How long have you been in business? Ensure they’re accredited and meet the Aged Care Quality and Safety Commission Standards.

- Will you involve my loved ones and me in care decisions? Your preferences and goals should guide your care plan.

- Will you ensure a good match between me and my carer? Consider language, personality, and interests.

- Will I receive care from the same people? Continuity of care is vital for trust and comfort.

- Do you directly employ or contract workers? Direct employment often ensures better training and accountability.

- What qualifications and training do carers have? Confirm they’re well-trained and regularly assessed.

- Do you conduct a home visit before starting? A care manager should assess your specific needs in person.

- What do your customers say? Look for transparent testimonials and reviews.

- What if I’m unhappy with my carer? Ensure there’s a clear and effective complaints process.

Talk to an aged care consultant before making a life-changing decision

Staying in your home longer isn’t just about avoiding aged care facilities; it’s about living life on your own terms, with dignity, safety, and the proper support in place. With planning, quality advice, and access to the right programs, your home can remain in your castle, secure, familiar, and full of comfort.

Do you want help finding specific strategies or examples of how advice is tailored to each person’s situation? Don’t just source your information from Services Australia; it’s easy to get lost in the jargon. Contact the aged care consultants at Elliot Watson Financial Planning for professional aged care advice and create an actionable plan for your family’s future.

Disclaimer:

The information within, including tax, does not consider your personal circumstances and is general advice only. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information, you should consider its appropriateness regarding your objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. The views expressed in this publication are solely those of the author; they are not reflective or indicative of the licensee’s position and are not to be attributed to the licensee. They cannot be reproduced in any form without the author’s express written consent. Elliot Watson Financial Planning Pty Ltd and its advisers are Authorised Representatives of RI Advice Group Pty Ltd, ABN 23 001 774 125 AFSL 238429.

Article by Geoff McQueen – Provisional Financial Adviser

Relevant Articles