The 2026 Federal Budget introduced a broad range of proposed measures affecting taxation, investments, property,…

How much super do I need to retire?

If you have ever asked yourself, “How much super do I need to retire?” you’re not alone. It’s one of the most common retirement questions Australians ask, and the answer depends on the lifestyle you want, not just your age or income.

As a starting point, the ASFA Retirement Standard suggests that, in today’s dollars, a single person needs around $595,000 in super for a comfortable retirement at 67, while a couple needs around $690,000. A more modest retirement can be achieved with far less, often with support from the Age Pension.

Here, we’ll explain what those numbers mean, how your current super balance compares, and how to estimate the amount you may need to retire with confidence.

Back to basics: what is superannuation, and why does it matter?

Superannuation is money set aside during your working life to fund your retirement income.

Your employer pays contributions into your super account, which is invested in a super fund and grows over time through returns and additional contributions.

Because super relies on long-term growth and compound interest, small changes today can make a big difference to how much money you have at retirement age.

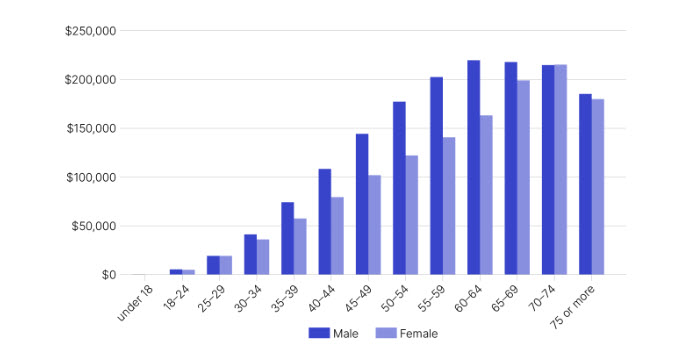

How much super should I have at my age?

There is no perfect super balance for every age group. However, average balances can help you sense-check where you are tracking. According to Australian Taxation Office data (latest published figures from the 2022/2023 financial year), average super balances look like this:

Image: Australian Tax Office

These figures show the average balance, not a target. They reflect what Australians actually have, not what they need to retire comfortably.

For example, if you are asking “How much super should I have at 30 or 50?”, the average balance is relatively low. That’s normal. What matters more is whether your balance is growing steadily and whether you are on track relative to your income and goals.

How average balances compare to ASFA targets

This is where the gap becomes clearer.

ASFA suggests that to maintain a comfortable retirement, you need significantly more than the average balance held by people nearing retirement. Most Australians retire with less super than ASFA recommends, which can affect living standards later in life.

A modest retirement is designed to cover basic living costs. Think limited budget, home delivery meals on an infrequent basis, modest wardrobe updates, local club special meals, a little discretionary spending, and so on.

A comfortable retirement allows for higher retirement income, private health insurance, a reasonable car, home repairs, dining at inexpensive restaurants, one overseas trip every few years, and a generally good standard of living.

The gap between averages and targets often means relying more heavily on the Age Pension, adjusting your spending in retirement, or making additional contributions earlier.

How much super does a couple need to retire?

Image: Pexels

For couples who own their home outright, ASFA estimates the following annual living costs in today’s dollars:

- Modest retirement: Around $50,866 a year

- Comfortable retirement: Around $76,505 a year

For singles, the figures are lower, but the same principles apply.

Rather than focusing on the full tables, the key takeaway is this: a couple does not need a million dollars to retire, but they do need enough superannuation and other savings to support their desired lifestyle, combined with any Age Pension eligibility.

Quick check: are you on track?

A simple rule of thumb is to aim for super savings of around six to eight times your annual income by retirement age for a comfortable retirement. This is only an estimate and does not replace personalised advice.

To refine your own number, try our calculators to estimate your target based on your personal circumstances:

How to determine how much super you need to retire

Instead of guessing, break it down step by step:

- Estimate your retirement spending: Consider what you want to spend on living, health insurance, travel, take-away meals, and hobbies.

- Subtract likely income: Include expected Age Pension benefits, other income sources, or investments outside super.

- Identify the gap: This is the amount your super balance needs to fund.

- Plan contributions: Review employer contributions, salary sacrifice, tax deduction opportunities, and additional contributions.

Key factors that shape your retirement number

Image: Pexels

Your lifestyle goals

Ask yourself what living standards you want. Will you travel overseas? Eat out regularly? Help the family financially? Your desired lifestyle drives how much super you need to retire.

Your mortgage and housing costs

Consider whether your home will be owned outright. Ongoing mortgage repayments, rent, or major home repairs can significantly increase the amount you need to retire.

Starting early and compounding

Compound growth rewards time. For example, an extra $5,000 contributed at age 30 could grow to more than $25,000 by age 65, assuming long-term returns. The same contribution at age 50 has far less time to grow.

Starting early, reviewing your insurance cover, and managing fees inside your super account can materially change your future balance.

Knowing how much super you need is about clarity, not perfection

Elliot Watson Financial Planning can help you review your super fund, contributions strategy, and retirement income plan so your savings support the life you want to live.

It’s important to note that the figures in this article are general information only, based on ASFA and publicly available data, and are expressed in today’s dollars. They don’t take into account your personal circumstances and are not personal financial advice. If you would like tailored advice, speak with our qualified financial advisers before making decisions about your superannuation and retirement.

Disclaimer:

The information within, including tax, does not consider your personal circumstances and is general advice only. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information, you should consider its appropriateness regarding your objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. The views expressed in this publication are solely those of the author; they are not reflective or indicative of the licensee’s position and are not to be attributed to the licensee. They cannot be reproduced in any form without the author’s express written consent. Elliot Watson Financial Planning Pty Ltd and its advisers are Authorised Representatives of RI Advice Group Pty Ltd, ABN 23 001 774 125 AFSL 238429.

Relevant Articles