The 2026 Federal Budget introduced a broad range of proposed measures affecting taxation, investments, property,…

Barefoot Investor – There IS Value in Advice

Book Review

‘The Barefoot Investor – The Only Money Guide You’ll Ever Need’ has sold over a million copies indicating there is a strong desire for Australians to be more financially literate. This is not surprising considering a 2016 MLC White Paper found that maintaining their lifestyle and financial security are the top priorities of Australians[1]. The same study found however that two in five (43%) did not believe they would be able to fund their lives post work.

As a Certified Financial Planner with over 14 years’ experience, I have had over a thousand meetings with everyday Australians looking to regain control of their finances and get ahead. The Barefoot Investor contains many great tips however, there is one recurring theme within the book that I think is dangerous and misleading. The book does not talk about the benefits of receiving quality financial advice, in fact, it advises against it. The Barefoot Investor, Mr Scott Pape, a financial adviser himself, recommends that you do not seek advice from a financial adviser, a solicitor and many other professionals. Instead he focuses on not spending money on advice and recommends garnering free financial advice from such places as Centrelink and the Public Trustee. Quite frankly this is crazy talk and let us explain why…

The book provides a thorough but cookie cutter approach to finances. This is where the problem starts. Each person’s or family’s financial circumstances are different, which is why financial planners work hard to develop tailored plans for their clients, getting to know their finances and aspirations intimately. If all Australians followed the book there would be some who would be significantly worse off than they were before. “Noooo”, I hear you say. “How is that possible”? Let us explain.

Mortgage v Savings

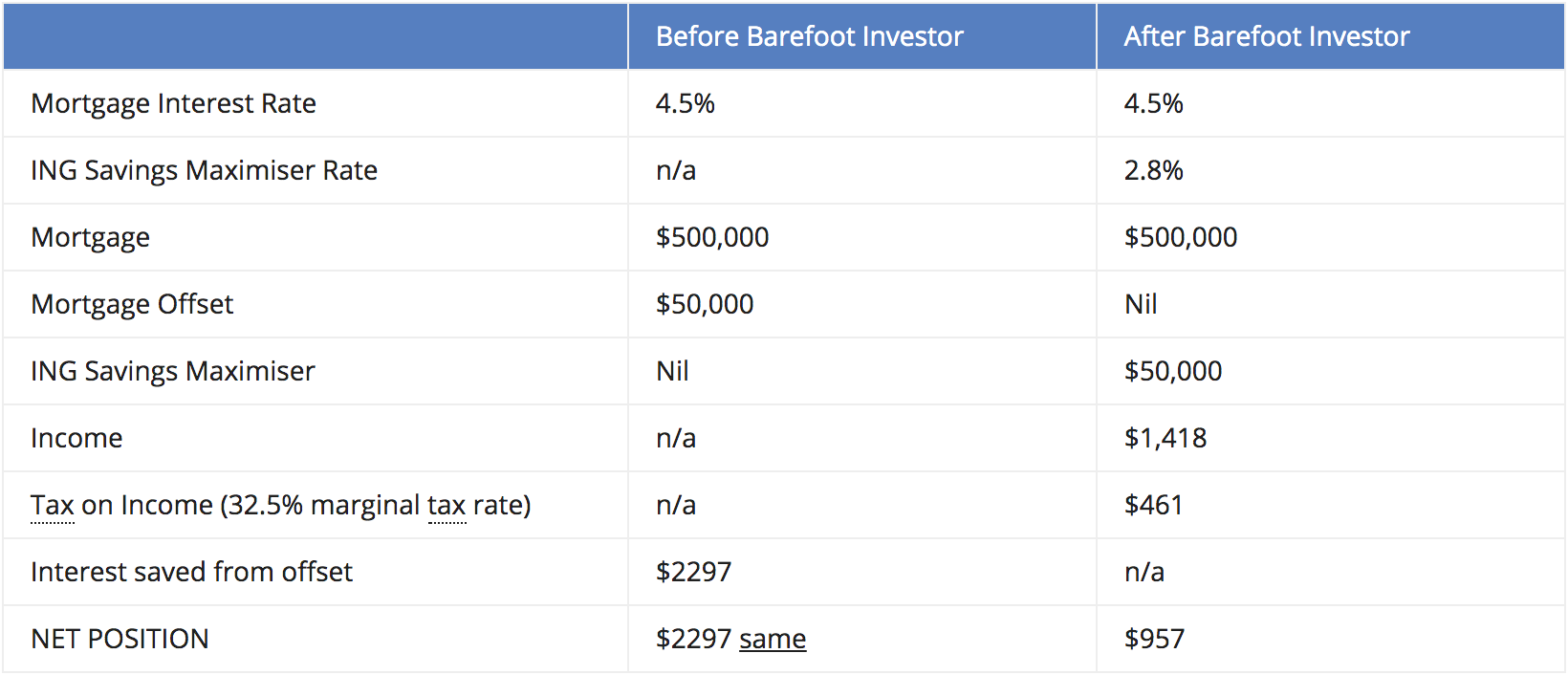

Justine and David followed everything that was recommended in The Barefoot Investor. They set up their ING Direct accounts and moved their money into the savings maximisers to make their “buckets”. Previously they had their excess cash in offset accounts connected to their mortgage. By moving their money Justine and David were worse off each year. The ING Direct accounts generated assessable income, which was added to their tax bill. Once income tax was taken out the net benefit of moving their funds as the Barefoot Investor advised was $957 per year. Had they kept their $50,000 in offset accounts they would have saved $2,297 per year in interest. Over the course of their loan their offset account would save them $89,921 in interest and knock 2 years and 7 months of the life of their loan.

https://www.ing.com.au/home-loans/calculators/offset.html

In the first year Justine and David are worse off by $1,340. Multiple this over life of the mortgage and they are tens of thousands of dollars worse off. A professional financial adviser would have done this calculation and made their clients aware of the best course of action and if they had read the Barefoot investor would also be able to prevent them by making such a mistake. The value of personalised financial advice in this context is worth $90,000 and a saving of 2 years and 7 months of time.

Retirement

Again, the Barefoot Investor says do not listen to financial advisers who say you need $1 million to retire. He reassures readers that they need not panic about their super balances, they only need $250,000 for a couple and $170,000 for a single. This is possible by utilising a strategy which maximises the age pension and uses the required 5 per cent draw down of superannuation each year. It is irresponsible and risky to promote this. Sure, it can be reassuring for a pre-retiree with little super, but any person younger than 50 should be aiming to have significantly more super, or retirement savings, than what the Barefoot Investor has recommended.

There are many things wrong with this claim, but let’s start with the most glaringly obvious – what KIND of retirement would these people have? The Barefoot Investor rattles off a list of things that you would be able to afford to do, like a 3-week trip to Noosa each year, from living off the aged pension and your ‘limited super’. However, here is the kicker, he wants you to keep working. In all my years of working with pre-retirees very few are excited by the prospect of still working. In a lot of cases, if they want to keep contributing, they want to do that by way of community service i.e. a non-paying job.

The Australian Super Fund Association (ASFA) has bench marked what a modest and comfortable lifestyle looks like in retirement. Using the Barefoot investor theory, if a 67-year-old retired with $170,000 in superannuation. They would have an estimated annual income of $31,121. A couple would have $46,633 per year till they are 90 years old, then they would just have the pension. Both are significantly below what is deemed a by the ASFA as a ‘comfortable’ lifestyle.

https://www.superannuation.asn.au/resources/retirement-standard

A modest retirement lifestyle is considered better than the Age Pension, but still only able to afford fairly basic activities. A comfortable retirement lifestyle enables an older, healthy retiree to be involved in a broad range of leisure and recreational activities and to have a good standard of living through the purchase of such things as; household goods, private health insurance, a reasonable car, good clothes, a range of electronic equipment, and domestic and occasionally international holiday travel.

https://www.moneysmart.gov.au/tools-and-resources/calculators-and-apps/retirement-planner

To get you to the ‘comfortable’ target the Barefoot Investor wants you to keep working. To be fair, it’s not much, one day a fortnight for you and your partner, however as mentioned before this doesn’t suit many people’s retirement dreams. Not to mention their bodies. These are 67-year old retirees we are talking about, not 55-year-olds. People who have potentially laboured all the lives and their bodies quite frankly are worn out.

In my experience retirees want to travel the world, travel around Australia in a caravan (which they need to buy and a car to tow it), they want to spend time playing golf and looking after their grandkids. Working is not usually on their list. Instead, if you look at what a lot of financial advisers recommend, having $1 million per couple, then they would have approximately $66,453per year. That amount of tax-free money can provide a significant difference in the quality of lifestyle in retirement. It’s the difference between being able to afford overseas holidays or having to keep working which is unappealing to most. It is subjective, but from my experience clients want to achieve a lot in their retirement, not be financially constrained after working all their life.

The Barefoot Investor’s advice also doesn’t factor in one huge risk which is the Australian Government changing the eligibility rules for the Age Pension. In the last ten years both sides of politics have made major changes to the Age Pension. All of which either resulted in a smaller pension (for most individuals) and/or made it harder and longer to qualify for the Age Pension. The more superannuation you have the less vulnerable you are to changes to the Age Pension.

At the end of the day all Australians need to save for their retirement. The sooner they start the better. Research shows if you seek expert advice from a financial adviser, you will be better off. In a 2018 study ‘Value of Advice’ by Core Data[2] it was found that everyday Australians who received financial advice confirmed that it added tangible value to their assets in retirement and peace of mind. Of those who received advice, almost 83% said they felt very well or reasonably well financially prepared for retirement. Of those who do not seek financial advice, only 33% felt they were financially prepared. Likewise, in a 2017 study by Sunsuper[3], of those currently advised 80% said they felt more confident making financial decisions as a result and the same proportion believe advice has brought them more peace of mind. Importantly 75% believed that financial advice is worth more than it costs. Again, there IS value in personalised financial advice.

Where You Put Your Superannuation and Insurance

Another area that we disagree with the Barefoot Investor is where to put your superannuation. He says “ultra-dirt cheap” is the way to go. He is right that these funds are low fee, but it is because they are low frills, low service and are usually run automatically by computers (passive investments). Importantly, they are not as agile with movements in the market as funds run by humans (active managers who lookout for opportunities and risks to your capital).

There is a fundamental issue with how superannuation’s funds are assessed. When we discuss projections, we always use the same rate of return which means the only true differentiation can be price (fees). This does not represent real results. We know when looking at returns no investment fund returns the exact same amount. This creates a paradox when trying to analyse such comparisons and an opportunity for the Barefoot Investor to focus on “ultra-dirt cheap” funds when comparing superannuation products because he is only looking at the superannuation fees. There is always a difference. The difference can be for good reasons or for bad reasons because a fund (or investment) has taken too much risk or sometimes because the market isn’t behaving rationally. When you have a fund doing extremely well over medium to long periods of time it is usually because they have a clear strategy.

The below table shows the real results of six ‘high growth’ funds over the past 10 years. You will notice firstly that none of the funds had the same return. You will also notice that the funds with the higher fees also had a higher return. It is therefore important to not purely make your investment decision on where to put your money based one variable i.e. low fees. Magellan Global is a fund with a strong proven track record of over 10 years. It charges much more than the dirt-cheap superannuation funds but as a result of its clear strategy it has performed well for the last ten years.

Calculated using: https://www.moneysmart.gov.au/tools-and-resources/calculators-and-apps/superannuation-calculator

Calculated using a starting investment balance of $0. Comparing six funds that are high growth funds. Assumed the investor has annual income of $85,000 per annum and superannuation guarantee (SGC) of 9.50%. High Growth means most of the investments are in. Australian shares, international shares and property.

A financial planner is legally obligated to do due diligence when making recommendations on where to invest your superannuation. They are required to provide you with a table that shows you the fees and costs associated with your existing superfund and alternatives. Below is an example of such a table.

Superannuation Comparison Table

The point to be made, like with all things, is you get what you pay for. Dirt cheap can also mean low value. Quality and value are essential in any investment portfolio. A financial adviser can design a portfolio that is appropriate to your specific needs and objectives, for example, tailoring a more defensive portfolio for retirees and a high growth fund for those with longer investment timeframes.Option 1 Super Fund allows you to have 50% of your funds invested in passive index funds and 50% invested in active alpha seeking funds.

Insurance

Insurance is another example of you get what you pay for. Insurance within superannuation can place you into ‘group insurance’ which does not consider you as an individual and any specific needs. Do not contact your industry fund for insurance advice, as recommended by the Barefoot Investor, they are not qualified or even allowed to give you insurance advice. There is value in getting personalise advice especially when it comes to pre-existing conditions and dangerous employment classifications. Elliot Watson Financial Planning was the Risk Practice of the Year in 2018 and has lots of experience with providing clients with sound insurance advice. If you don’t pay now, you will most likely end up paying at claim time.

So, Who Should You Seek Advice From?

It is advisable to seek financial advice from a Certified Financial Planner, who are experts in their field. Yes, you will need to pay for the advice, as nothing is free but as we have spelled out in this article, there are many benefits that tailored financial advice can provide which in our opinion far out way the costs. Following a cook cutter approach is dangerous and does not take into account your individual needs or the needs of your family.

[1] https://www.mlc.com.au/content/dam/mlc/documents/pdf/retirement/save-retirement-white-paper-part2.pdf

[2] 2018 Value of Advice, CoreData and AFA

[3] 2017 Value of Advice Report, Sunsuper

The information within, including tax, does not consider your personal circumstances and is general advice only. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser.

The views expressed in this publication are solely those of the author; they are not reflective or indicative of licensee’s position and are not to be attributed to the licensee. They cannot be reproduced in any form without the express written consent of the author.

Elliot Watson Financial Planning Pty Ltd and its advisers are Authorised Representatives of RI Advice Group Pty Ltd, ABN 23 001 774 125 AFSL 238429.

Relevant Articles